Lights out (Iran Edition)

![]() Lights out (Iran Edition)

Lights out (Iran Edition)

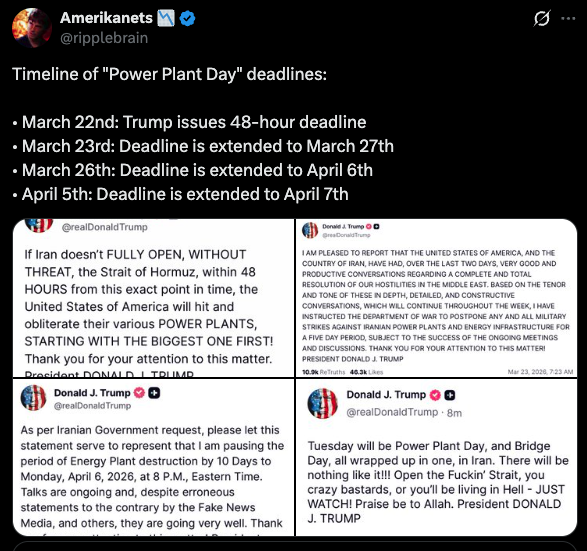

The latest deadline for the start of U.S. attacks on Iran’s power grid is 8:00 p.m. EDT tomorrow night.

The latest deadline for the start of U.S. attacks on Iran’s power grid is 8:00 p.m. EDT tomorrow night.

Subject to change, that is…

The current deadline is attached to a demand that Tehran reopen the Strait of Hormuz — which we’ll remind you was open for all to transit before Washington and Tel Aviv launched this war.

Should the president follow through, the Iranian response will be severe.

“Iran will retaliate and destroy critical power plants in nations where US forces are operating,” writes ex-Navy SEAL Matthew Bracken. That includes Kuwait and Saudi Arabia.

“Iran is 95% water self-sufficient. On the other side of the Persian Gulf they are 90% dependent on desalinated water. Millions may perish from lack of water. It will be impossible to fly them all out in time to prevent a massive human disaster.”

But about the electricity…

“Iran's power grid is very robust and redundant compared to the American grid,” Bracken writes on his Substack page.

“90% of Iranian households are connected to gas pipelines and a mostly gas-powered electric grid. Iran's natural gas is virtually unlimited for many decades to come. Destroyed sections of natural gas pipelines can be fixed in hours, or days at most. Gas and electricity can be rerouted around Iran's vast interconnected grids as individual power plants are struck, and then repaired.

“Iran’s gas and electric grid networks were designed this way for a purpose. The eight-year war from 1980–1988 is not a distant memory. Iran has remained on a war footing ever since, planning for damage control.”

In contrast, “the USA is far more vulnerable to catastrophic cascading power failure than Iran,” Bracken continues.

He invokes the still-unsolved sniper attack in 2013 targeting the Metcalf transmission substation near San Jose, California — operated by Pacific Gas and Electric. The saboteurs fired on 17 electrical transformers.

The impact on the grid was minimal — as electricity was rerouted from other power plants around Silicon Valley. But by many accounts, that was just a lucky break.

“10 Metcalf attacks at the same time could take out the power across entire regions of America,” Bracken writes.

That’s not hyperbole — as we’ve chronicled previously. The same year as the Metcalf attack, the Federal Energy Regulatory Commission performed a computer-model stress test of the national power grid.

The findings were summarized in a memo prepared for the FERC's commissioner: "Destroy nine interconnection substations and a transformer manufacturer and the entire United States grid would be down for at least 18 months, probably longer."

That’s just nine substations out of 55,000 total nationwide.

The good news is that leaders in Tehran know how unpopular this war is in the United States. The last thing they’d want to do at this time is anything that would create a “rally ’round the flag” effect.

Unfortunately, all the problems that existed with the U.S. power grid before the war remain. An update about that is coming in Bullet No. 3.

But for the moment, we turn to the latest war developments and the markets today…

![]() If It’s Monday, It Must Be Ceasefire Buzz…

If It’s Monday, It Must Be Ceasefire Buzz…

Threats notwithstanding, it seems the market is pricing in another TACO — which, to refresh your memory, is short for “Trump always chickens out.”

It being Monday, there’s renewed chatter from Washington about a ceasefire — chatter that Tehran denies has any validity.

Crude shot higher as the new week began last night — past $115 briefly — but at last check a barrel of West Texas Intermediate is now down slightly from Friday’s close at $111.26.

But those are oil futures — “paper barrels,” as it were. Real barrels being delivered to Asian refiners cost anywhere between $130-170, according to Carlyle Group’s Jeff Currie.

When it comes to commodities, Currie is a vital voice outside of Paradigm that we follow closely.

“You look at the paper markets, they’ve entirely disconnected from the physical markets,” Currie told Bloomberg TV last Thursday.

“The supply shock [now] is almost equal to the demand shock during COVID. And we know what that did to global supply chains. So I think at $100 a barrel, this thing’s mispriced.”

In the meantime, more vessels are transiting the “tollbooth” that Iran has erected in the Strait of Hormuz.

“Traffic through the Strait of Hormuz has climbed to its highest levels since the early days of the war, as more countries secure apparent safe-passage agreements with Iran,” Bloomberg reports. “The waterway saw 21 ships transit over the weekend.”

But that’s still a far cry from the prewar daily average of 135 ships. Analysts at Morgan Stanley project the strait will be more or less shut through the end of this month.

Amid that backdrop, the ceasefire chatter is driving the major U.S. stock indexes up slightly from last week’s close.

The S&P 500 is up a little less than a quarter percent, about four points shy of 6,600 — the highest since March 19, The Dow and the Nasdaq are also in the green.

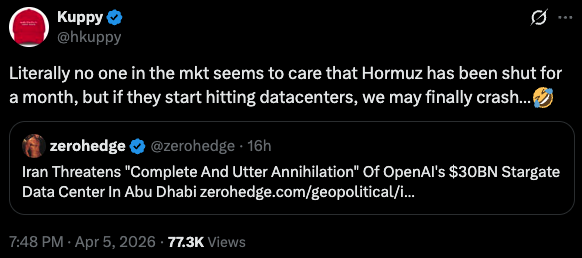

The stock market’s seeming indifference to the disruption in global oil flows brought forth this bit of grim humor…

Gold begins the new week down slightly at $4,665 and silver down about 1% at $72.19. Crypto is staging a modest rally — Bitcoin less than $300 away from the $70,000 mark again and Ethereum at $2,165.

Speaking of data centers…

![]() About That Data Center Buildout…

About That Data Center Buildout…

The breakneck buildout of data centers is running into severe real-world restraints — namely a lack of transformers.

“Almost half of the U.S. data centers planned for this year are expected to be delayed or canceled,” warns a Bloomberg dispatch. “One big reason is the shortage of electrical equipment, such as transformers, switchgear and batteries.”

That gear accounts for only about 10% of a data center’s total cost — but “if one piece of your supply chain is delayed, then your whole project can’t deliver,” says Andrew Likens of Crusoe Energy Systems.

Privately held Crusoe is a fortunate exception to the rule: It managed to secure enough gear that it expects to complete a data center campus on schedule for OpenAI in Abilene, Texas.

This supply crunch affects not only data center construction but the buildout of the power grid necessary to support those data centers.

We saw it coming nearly a year ago: The North American Electric Reliability Corporation warned last May that a shortage of “parts, materials and skilled technicians” is holding up both maintenance of existing transformers and installation of new ones.

“We can talk about tens of gigawatts of new potential electricity demand,” energy journalist Robert Bryce told the Financial Sense podcast — “but if we don't have the turbines, transformers and the people to build the capacity, well, that simply won't be realized. That capacity, that new electricity availability, just simply won't be there.”

Ironically the slowdown in data center construction might put a crimp in projected electric demand as the year goes on.

But the long-term supply crunch remains real. Most of the biggest power transformers are imported. And many of the most important parts come from China.

![]() Follow-up: Private Credit

Follow-up: Private Credit

For the record: JPMorgan Chase CEO Jamie Dimon warns that losses from private credit will be greater than much of Wall Street expects.

We’ve been sounding the alarm about private credit for the last six months — most recently Friday with the help of Paradigm macro authority Jim Rickards.

As a refresher, private credit is a term covering a wide variety of loans that used to be offered by banks but now are offered by the likes of Blackstone, Apollo and KKR.

Many of these private credit providers lent to companies with high levels of debt relative to their earnings — and they’re now sitting on losses. In some cases these providers have prevented investors in these loans from withdrawing their funds.

In his annual shareholder letter, Dimon warns: “I do believe that when we have a credit cycle, which will happen one day, losses on all leveraged lending in general will be higher than expected, relative to the environment… This is because credit standards have been modestly weakening pretty much across the board.”

Yes, Dimon represents everything wrong with our “financialized” economy that relies on moving money around instead of creating new wealth… but we’ll take his warning at face value here.

![]() Mailbag: SpaceX and Market Manias

Mailbag: SpaceX and Market Manias

After Thursday’s edition in which we briefly unpacked the case against buying SpaceX once it goes public…

… we heard from a reader who says. “I’m a 60-year-old certified management accountant. I’ve been involved with several M&A transactions and currently have a minority equity stake in a group of businesses that does around $200 million in revenue.

“When I hear that an IPO is valued at 117X revenues ($1.75 trillion versus $15 billion) this is a clear sign that we are in mania territory.

“You guys are usually straight shooters but I’m disappointed that you weren’t more explicit in your denouncement of this deal. In the real world, guys like me analyze earnings (not revenue) as proper fundamental technical analysis. And we mortgage our houses to make deals for companies that are 3–6 times earnings not 117X revenues. You want to get laughed out of my office, come to me with that deal.

“I understand new tech and IP, and Space X is not that… it is a well-established company with years of financial reporting (albeit internal not external).

“My humble opinion is that people are going to lose their shirts if they invest in this IPO. Now, I think that you guys try to look after your customers but I’m disappointed that you’re not more explicitly pointing out that we’re clearly in a mania. Somehow it has become normalized that future revenues have become recognized as a valid way of valuing a company which is complete bollocks unless you are talking about a true new technology IPO.

“OK, rant over. I’m worried about what happens to people when this bubble bursts. Please do what you can with your team to prepare them for the worst if it happens.”

Dave responds: Thank you for sharing your concerns. It’s rare when a reader calls us out for not being emphatic enough!

My colleague Davis Wilson expanded on his case against SpaceX in Friday’s edition of The Million Mission. Drawing on his experience in investment banking, he concludes, “Great companies and great investments are not the same thing” — and with that in mind he urges readers in no uncertain terms to “stay AWAY from this IPO.”

As for the broader issue of a “mania” or “bubble”... the problem is that manias and bubbles can go on way longer than sober-minded folks like you and me reasonably expect.

Lots of very smart people bailed from the dot-com boom and took profits at the end of 1998 — missing out as the Nasdaq proceeded to double over the next 14 months.

I suspect many of those people slept soundly and did not kick themselves for the profits they gave up. But that’s because they were very early to the party and already booked huge gains.

As editors and publishers, we have an exceedingly tricky task — mindful that even as a mania or bubble is underway, we’re also writing for an audience of retail investors, many of whom were not early to the party and who will not forgive us readily if our guidance leads them to miss out on 1999-style gains.

So we collectively watch everything from company fundamentals to chart action to events in Washington. At this time it’s the assessment of our chief investment director Enrique Abeyta that the “mania” is not yet approaching its end.

But he — and all of us — are on watch for signs telling us when it is. So stay tuned…

")

")

")

")

")

")

")

")